Today, the biggest news comes from Russia.

Here, Russia’s spending is reaching heights not seen since the fall of the Soviet Union, while oil and gas revenues are dropping at a record pace. With internal economies crumbling, Russia is approaching a financial breaking point that its own analysts now describe as a four-month countdown to systemic failure.

Russian financial officials have informed Vladimir Putin that the country may face a major financial crisis within 4 months. High interest rates and rising inflation are converging into a pressure point that officials believe could become unmanageable before the summer.

This reversal follows a short‑lived consumption boom driven by large signing bonuses, death payouts, and higher wages in war‑related industries, which temporarily injected significant cash into traditionally poorer households. The sudden liquidity fueled the opening of new restaurants, small luxury shops, and service businesses, as entire rural and provincial economies came to revolve around these wartime payouts. However, the crutch is that these cash insertions are one-off, and once they are spent, the money is gone.

At the same time, major defense industries are struggling despite massive state funding; as you may recall, factories such as Russia’s main tank producer, Uralvagonzavod, have laid off between 10 and 50 percent of their workforce due to a lack of orders. With one‑off payouts exhausted and key producers scaling back activity, the micro‑economies sustained by this cash flow are collapsing.

Early indicators of this breakdown are already visible, including a wave of restaurant closures in cities and layoffs across service sectors. These trends reflect weakening consumer demand and tightening credit conditions, both of which are steadily eroding the government’s income and fiscal room to maneuver, being compounded by falling revenue in the energy export sector.

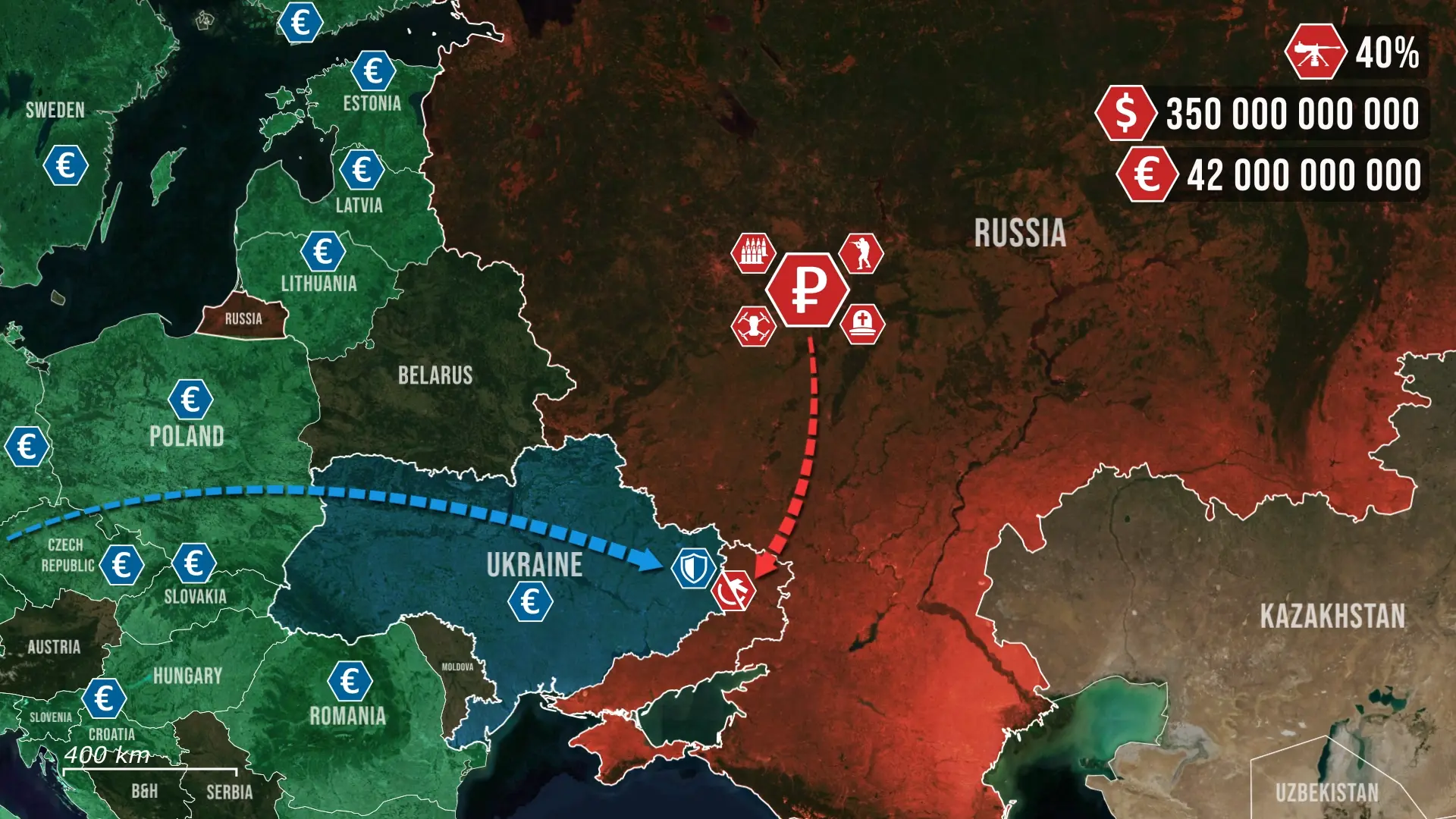

Before the war, oil and gas accounted for 40 to 50 percent of Russia’s federal budget revenue. However, current estimates suggest this share has dropped to about 22 percent. Several factors contribute to this decline, such as sanctions that have reduced access to Western markets and increased controls on maritime transport to counter Russia’s shadow fleet. In a recent turn, India has reduced purchases of Russian crude by nearly 30 percent, causing Russia to store an estimated 140 million barrels of unsold oil on tankers. January revenue figures indicate the lowest energy income in five years, down by half compared with the same month in the previous year, thereby removing the primary buffer that had historically allowed the Kremlin to absorb economic shocks.

In the meantime, Russia’s military spending has reached its highest level in decades, with approximately 40 percent of the national budget now allocated to defense and security. These funds support ammunition production, drone procurement, payments to contract soldiers, and compensation for casualties. As of now, Russia’s war expenditures accelerated dramatically, reaching a staggering figure of 350 billion dollars this year. As a result, Russia’s reserve fund has fallen to half of its pre-war level, now being only roughly 42 billion euros, reflecting the speed at which the Kremlin is drawing down assets to cover military costs. Despite this spending and economic mobilization, Russia is not securing any decisive strategic or tactical gains on the battlefield, while the cost of sustaining operations continues to rise. The imbalance between expenditure and battlefield outcomes is becoming a structural liability, particularly as Ukraine and its partners maintain a more resilient funding base, even though the combined war expenditure to date is less than Russia's.

Record-low revenue, combined with record-high spending, creates a structural deficit that is widening faster than the government can offset through taxation or borrowing. If the projected crisis materializes, Russia could face a banking shock triggered by depositor flight, a sharp devaluation of the ruble, and forced cuts to civilian spending.

Inflation would accelerate as the government prints money to cover obligations, and regional budgets would struggle to maintain basic services. The cumulative effect would be a contraction in economic activity that fundamentally undermines both Russia’s domestic stability and its ability to sustain the war effort.

Overall, the emerging picture is one of a state approaching the limits of its financial ability. The warning from Russian officials reflects not only immediate fiscal pressures but also the long‑term consequences of sustaining a high‑intensity conflict with diminishing revenue sources. The broader implication is that Russia’s economic trajectory is becoming increasingly dependent on external actors, particularly those in Asia, which introduces strategic constraints of its own. The situation suggests that even without a sudden collapse in four months, the structural weaknesses now visible will shape Russia’s options for years to come.

.jpg)

Comments